The PRESS RELEASE copied below on the global trade implications of COVID-19 was prepared by the Division on International Trade and Commodities, UNCTAD for global release on 4 March 2020.

OVERVIEW

“It is unavoidable that the novel coronavirus epidemic will have a considerable impact on the economy and society” – China’s president Xi Jinping, televised address, February 23, 2020.

“The spread of the new coronavirus is a public health crisis that could pose a serious risk to the macro economy through the halt in production activities, interruptions of people’s movement and cut-off of supply chains” – Japanese Finance Minister Taro Aso. G20 gathering in Riyadh, Saudi Arabia, February 24, 2020.

“Honda Motor Co. will reduce vehicle output at two of its domestic plants in Saitama Prefecture for a week or so in March due to concerns about parts supply from China where a new coronavirus outbreak continues to disrupt economic activities” – Honda spokesperson, March 3, 2020.

Besides its worrying effects on human life, the novel strain of coronavirus (COVID-19) has the potential to significantly slowdown not only the Chinese economy but also the global economy. China has become the central manufacturing hub of many global business operations. Any disruption of China’s output is expected to have repercussions elsewhere through regional and global value chains.

Indeed, most recent data from China indicate a substantial decline in output. China Manufacturing Purchasing Manager’s Index (PMI), a critical production index, fell by about 22 points in February (Figure 1a). This index is highly correlated with exports and such a decline implies a reduction in exports of about 2 percent on an annualized basis. In other words, the drop observed in February spread over the year is equivalent to -2 percent of the supply of intermediate goods. Indicators on shipping also suggest a reduction in Chinese exports for the month of February (Figure 1b). Container vessel departures from Shanghai were substantially lower in the first half of February with an increase in the second half. However, the Shanghai Containerized Freight Index continues its decline thus indicating excess shipping capacity and lower demand for container vessels.

ANALYSIS METHODOLOGY

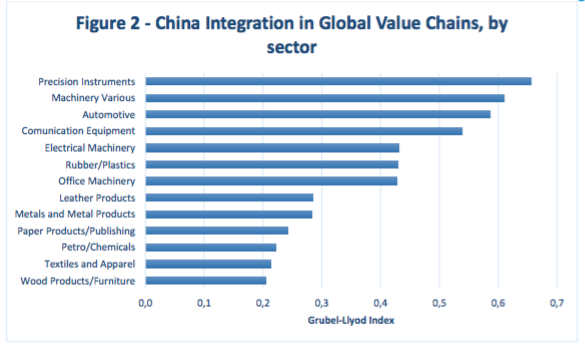

The methods used in this note are meant to identify the economic sectors and countries that are most exposed to a disruption of China’s exports of intermediate inputs. The analysis is based on United Nations Statistics Division trade data covering about 200 countries and 13 manufacturing sectors. In summary, each country’s and industry’s integration with the Chinese economy is measured by the Grubel-Lloyd Index (GLI) of intra-industry trade. The GLI is calculated on products categorized as manufacturing intermediate inputs (e.g. parts and components), computed at the industry level (as defined by the 4 digit Harmonized System classification) and then aggregated at the sectoral level using bilateral trade shares. The GLI is then used as a proxy measuring the percentage of a given country’s exports in each industry that is vulnerable to supply disruption in China.

Notably, the analysis assumes that supply disruptions are limited to China. Disruptions that COVID-19 may directly cause in the output of other countries are not considered at this stage. The results of the analysis are to be interpreted as short-term effects as they assume the supply capacity in the rest of the world to remain constant. This note does not consider commodities and minerals (e.g. rare earths) but focuses only on manufacturing output. Finally, this note does not examine the impact of reduced remand due to any economic slowdown in China (e.g. impact on third country of the reduced Chinese imports of commodities).

IMPACT ON GLOBAL VALUE CHAINS

During the last two decades, China has become crucial to the global economy. China’s rising importance in the global economy is not only related to its status as a manufacturer and exporter of consumer products. China has become the main supplier of intermediate inputs for manufacturing companies abroad. As of today, about 20 percent of global trade in manufacturing intermediate products originates in China (up from 4 percent in 2002).

Figure 2 shows China’s current integration in global value chains across sectors as measured by the GLI. Chinese manufacturing is essential to many global value chains, especially those related to precision instruments, machinery, automotive and communication equipment. Any significant disruption in China’s supply in these sectors is deemed to substantially affect producers in the rest of the world. Indeed, many companies around the world are fearful that the measures put in place to contain COVID-19 (i.e. restrictions to economic activities and movement of people), could hinder the supply of critical parts from Chinese producers, therefore affecting their own output.

IMPACTED COUNTRIES

A reduction in Chinese supply of intermediate inputs can affect the productive capacity and therefore the exports of any given country depending on how reliant its industries are on Chinese suppliers. For example, some European auto manufacturers may face the shortage of critical components for their operations, companies in Japan may find difficult to obtain parts necessary for the assembly of digital cameras, and so on. For many companies, the limited use of inventories brought by a lean and just-in-time manufacturing process would result in shortages that will impact their production capabilities and overall exports. Table 1 reports by sector the potential effect of COVID-19 on exports in the most exposed countries to Chinese supply disruptions. Overall, the most impacted economies will be the European Union (machinery, automotive, and chemicals), the United States (machinery, automotive, and precision instruments), Japan (machinery and automotive), the Republic of Korea (machinery and communication equipment), Taiwan Province of China (communication equipment and office machinery) and Viet Nam (communication equipment).

KEY POINTS

While there is still uncertainty about the impact of the COVID-19 on China’s productive capacity, the most recent statistics point to a significant downturn. The full effect of COVID-19 on global value chains will become clearer in the coming months. However, one question

of importance is how a disruption in Chinese supply of intermediate inputs will affect the rest of the world. Based on the analysis of this note, two key points can be made.

First, even if the outbreak of COVID-19 is contained mostly within China the fact that Chinese suppliers are critical for many companies around the world implies that any disruption in China will be also felt outside China’s borders. European, American and East Asian regional value chains will be disrupted. The estimated global effects are subject to change depending on the containment of the virus and or changes in the sources of supply.

Second, it is expected that the spillover effects of a disruption in Chinese supply will be diverse across economic sectors and dependent on the geographic localization of the COVID-19 outbreak and of the containment measures within China. For example, automotive industry’s intermediate exports may fall relatively more as the industry is geographically localized in the region where the outbreak of COVID-19 occurred. Importantly, because of lack of information this note does not consider this second aspect. Once sectoral data on Chinese output is available the likely effect on the various global value chains will become clearer.

")

{kind=link}